COVID-19 – Economic Support Packages in Response to the Coronavirus Impact and the Superannuation Measures Introduced

To date, $189 billion has been injected into the economy in order to keep Australians in work and businesses in business, including the first $17.6 billion package, the RBA and Government’s $105 billion to the banks to deliver easier access to finance, and the latest $66.1 billion stimulus package.

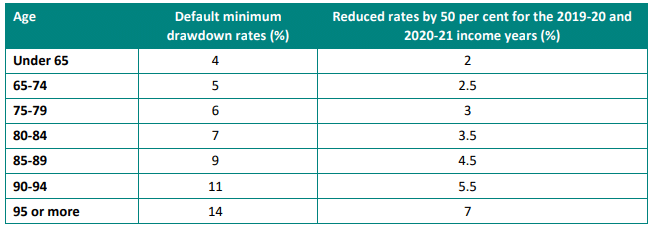

The government will also reduce the minimum pension drawdown requirements for account-based pensions and similar products by 50 per cent for the 2019–20 and 2020–21 financial years. This measure reduces the need for retirees to sell investment assets to fund minimum drawdown requirements.

Deeming rates for pensioners will also be reduced by another 0.25 of a percentage point.

Eligible individuals, including employees who have been made redundant or whose working hours have been reduced by >20%, those unemployed, and sole traders whose businesses have been suspended or seen a reduction in turnover by >20%, will be able to apply online through myGov to access up to $10,000 of their superannuation before 1 July 2020, and a further $10,000 from 1 July 2020 for approximately three months.

These important superannuation measures are explained in more detail below.

Temporary reductions in superannuation minimum drawdown rates

The Government is temporarily reducing superannuation minimum drawdown requirements for account-based pensions and similar products by 50% for the 2019-20 and 2020-21 financial years. This measure will benefit retirees by providing them with more flexibility as to how they manage their superannuation assets.

Individuals who have already taken their minimum pension amount for the 2019/20 financial year will not be able to put that money back into their superannuation account under these changes.

Reducing social security deeming rates

As of 1 May 2020, the upper deeming rate will be 2.25% and the lower deeming rate will be 0.25%. The reductions reflect the low interest rate environment and its impact on the income from savings.

The change will benefit around 900,000 income support recipients, including around 565,000 people on the Age Pension who will, on average, receive around $105 more from the Age Pension in the first full year that the reduced rates apply.

The changes will be effective from 1 May 2020.

For example

Leslie and Brian are an age pensioner couple. They have $550,000 worth of financial assets. They hold $300,000 in a superannuation account with a conservative investment strategy which returned around 5% last year. They have invested $130,000 in a term deposit with an annual return of 1.5% and hold the remainder in a cash transaction account earning a negligible rate of interest.

Under the former deeming rates, Leslie and Brian’s Age Pension would have been reduced by $65 each per fortnight. Under the new deeming rates, Leslie and Brian’s Age Pension will only be reduced by around $32 each per fortnight.

Early release of superannuation

While superannuation helps people save for retirement, the Government recognises that for those significantly financially affected by the Coronavirus, accessing some of their superannuation today may outweigh the benefits of maintaining those savings until retirement.

Eligible individuals will be able to apply online through myGov to access up to $10,000 of their superannuation before 1 July 2020. They will also be able to access up to a further $10,000 from 1 July 2020 for approximately three months (exact timing will depend on the passage of the relevant legislation).

The exact eligibility requirements will be formed in the coming days but broadly to apply for early release you must satisfy any one or more of the following requirements:

you are unemployed; or

you are eligible to receive a job seeker payment, youth allowance for jobseekers, parenting payment (which includes the single and partnered payments), special benefit or farm household allowance; or

on or after 1 January 2020:

you were made redundant; or

your working hours were reduced by 20 per cent or more; or

if you are a sole trader — your business was suspended or there was a reduction in your turnover of 20 per cent or more.

People accessing their superannuation will not need to pay tax on amounts released and the money they withdraw will not affect Centrelink or Veterans’ Affairs payments.

If you are eligible for this new ground of early release, you can apply directly to the ATO through the myGov website.

Separate arrangements will apply for members of a SMSF.

You will be able to apply for early release of your superannuation from mid-April 2020.

How can we help?

We will provide further updates that affect the superannuation industry as they become available. As our business operates online and our staff and auditors are working remotely within Australia, we do not foresee any major disruption to our service to you during this time, but will keep you informed if delays are expected.

Take care of yourselves, your families and each other.

Lodgement Performance FYE 30/06/2017

The ATO released the tax agent lodgement results for the 2017 year and we have achieved a 99% on-time lodgement performance result. The ATO’s benchmark is 85%. A big thank you to our clients, their advisors, our Green Frog Super team and our auditors for all your cooperation and assistance in helping to achieve this.

New Rules helping employees save tax in 2018 with Personal Super Contributions

With the eligibility conditions being relaxed on who can make personal, tax deductible (concessional) super contributions, it may be worthwhile to consider if you can benefit from the changes.

Prior to 1 July 2017, if you weren’t self-employed you were generally unable to make personal, tax-deductible contributions to super with your ‘take home’ pay. The only tax effective way to get extra money into super was to opt for salary sacrificing, which wasn’t always viable. Recently, changes have been made to super contributions to exclude the requirement that wages could not exceed 10% of your total assessable income. This means that from the 2018 financial year onwards, it is possible to reduce your personal tax by making deductible super contributions.

Scenario

As an example, Sarah has taxable income of $75,000, made up of $73,000 in wages and $2,000 in net investment income. In the past she would have been unable to make a personal deductible contribution to super because of the old 10% rule, but now she can.

Assuming she has $5,000 to contribute and receive a tax deduction for, her tax would be affected in the following ways:

Personal Tax Return

Super Fund’s Tax Return

$5,000 deduction

$5,000 contribution

Saves $1,725 in tax

Pays $750 in tax

Tax savings of 34.5%* (*32.5% marginal rate of tax + 2% Medicare levy)

Tax payable of 15%

Overall, she benefits by $975 and the contributed money would be in the superannuation environment where its earnings are taxed at 15% rather than the potentially higher personal marginal rates.

Other things to consider

From a tax perspective there is a benefit whenever the personal rate of tax is higher than the 15% rate of tax that the super fund will incur. However, there are other things to keep in mind when deciding whether or not it’s a good idea to make a voluntary personal contribution. These include:

Personal Liquidity/Future Access to the Money

Once money is contributed to super it cannot be easily withdrawn. If those funds are subsequently needed for personal use they cannot be accessed until a condition of release has been met. This is generally retirement after preservation age or turning 65 or if eligible for release under the First Home Super Saver Scheme*.

Concessional Contribution Cap

Currently there is a $25,000 limit to the amount of money that can be contributed to super where a tax deduction is being claimed by the contributor. These are referred to as concessional contributions and include:

Employer contributions

Any amount you salary sacrifice into super

Personal contributions you claim as a personal super contribution deduction

Consideration needs to be given to the total dollar value being contributed into super for the year on your behalf; not just the amount that qualifies for a personal tax deduction.

Tip: Consider also the timing of contributions. Often the employer will pay the June quarter contribution in June rather than in July when it is due. The timing of receipt into the Super Fund’s bank account affects the year in which it is counted towards the contribution cap and when it is available as a tax deduction. The contribution must be received by the super fund on or before 30 June for a deduction to be claimed in the same financial year.

Documentation Needed

If you want to claim a tax deduction your super fund needs to receive a completed Notice of intent to claim a deduction form within the required timeframe. You need to receive an acknowledgement of this notice before you lodge your tax return for the relevant year. Without that acknowledgement a tax deduction cannot be claimed.

If the contribution is being made to an industry or retail fund you may need to make enquiries regarding how they need to be notified of the personal concessional contribution.

If the contribution is being made to a SMSF you need to ensure that both the Notice of intent and acknowledgement forms are completed. These forms can be found on our website using the links below:

If you are under 18 years of age you can only claim a deduction for your personal super contributions if you earned income as an employee or a business operator; not as passive investment or distribution income.

If you are 75 years of age or older, you can only claim a deduction for contributions you made on or before the 28th day of the month following the month of your 75th birthday. There is also a work test for contributions made after turning 65.

*First Home Super Saver (FHSS) Scheme

From 1 July 2017 the FHSS Scheme allows people to save money for a first home inside their superannuation fund. A voluntary contribution to super, whether concessional (tax-deductible) or nonconcessional (non tax-deductible) may be able to be released at a later date if certain eligibility requirements are met. Further information can be obtained on the ATO website.

By Karen Barnes – Green Frog Super

Disclaimer:

We are not financial advisers. The information in this article is general in nature and does not constitute financial advice. It has been prepared without taking your personal circumstances into consideration. Before acting on any information you should assess or seek advice from a licenced financial adviser on whether it is appropriate for your situation and objectives.

Thinking of Setting Up a Self Managed Super Fund (SMSF)?

Did you know that you could save money by waiting until July before putting any assets into the fund?

This time of the year is typically a very busy time for the set-up of self-managed superannuation funds (SMSFs) as people review their financial and taxation positions and make decisions before the end of the financial year.

If you’ve decided to establish your own SMSF, give some consideration to whether you really need it up and running prior to 30 June or whether it can wait until July.

The decision could mean a savings of $1,600 or more if you can wait.

Let me explain.

To be legally established, not only must you sign various legal documents but the fund also needs to hold assets. The first asset held by a new fund is typically a bank account where a contribution or rollover is deposited into.

The financial year in which the first asset is held by the fund determines when a tax return and audit are required. So, if a bank account is opened and money deposited prior to 30 June 2018, there will be a requirement for a tax return and an independent auditor’s report for the 2017/18 year. This will entail some administration costs for the fund as outlined below:

ATO Supervisory Levy

$ 259.00

Independent Auditor

$ 395.00

Administration Fees

$ 950.00*

Total

$1,604.00

(the administration fees may be able to be negotiated lower for that first year; but a fee is still likely to apply to prepare the necessary documentation; liaise with the auditor and lodge the return)

If, however, the first assets held by the fund occurred from 1 July 2018 there would be no need to lodge a tax return or conduct an audit for the 2018 financial year.

There are other things to consider regarding the best time to set up your fund besides the administration and supervisory levy savings, but this is one aspect that is sometimes forgotten.

For more information about our set up service Click Here

Managing the new transfer balance cap for pensions – You now need to consider whether to treat payments as an income stream (normal pension payment) or a lump sum.

The transfer balance cap applies from 1 July 2017. It is a new limit on the total amount of superannuation that can be transferred into retirement phase and it is currently $1.6 million.

Why does it matter whether a payment is an income stream payment or a lump sum?

The short answer is that lump sums affect the transfer balance account; whilst income stream payments do not.

Perhaps the first thing that needs to be clarified is what is meant by taking a lump sum from a pension. Many people think this means taking a once-off or infrequent payment from their pension account rather than taking it, say, monthly or fortnightly. That sounds reasonable enough, but unfortunately that isn’t what is being referred to. A ‘lump sum’ relates to the intention and documentation surrounding a withdrawal; not the timing or frequency.

In the past, taking a lump sum after retirement was generally for Centrelink Age Pension reasons or for those under 60 who could utilise the low rate cap. As such, it was relatively uncommon to treat payments as a lump sum, especially for those over 60 and retired. The new transfer balance cap has changed that and it is likely that the taking of lump sums will become much more common.

Here’s an example of the different treatment between a lump sum payment and an income stream payment for cap purposes:

Scenario 1

On the 1st of July a pension is started with $1.6 million which fully utilises the cap. There is a $1.6 million credit to the transfer balance account that is reported to the ATO (This isn’t a bank account; it’s more like a ledger account that keeps track of transactions that affect the cap. Being under the cap is okay, but exceeding it will entail penalties). Because $1.6 million has been applied to the cap the person is not able to put any additional money into pension phase.

With $1.6 million in pension on the 1st of July the person needs to withdraw at least the minimum at some stage during the year. This could be a once-off annual payment, monthly payments or even ad hoc payments as they are needed. For a person that is 65 years old the minimum is 5% or $80,000. If only the minimum pension payment is going to be taken for the year then there’s no need to consider the lump sum strategy. That’s because that $80,000 has to be taken as a normal income stream payment to meet the minimum pension payment requirement. Lump sums no longer count towards the minimum pension payment effective 1 July 2017.

If, however, the person plans to take more than that during the year then a decision needs to be made about how to treat the excess over the $80k. Let’s say that $150k is needed.

Income Stream

We know that $80k of that has to be treated as an income stream payment. The extra $70k could be treated like that as well and that would not cause any compliance issues. In fact, if nothing is done, that $70k, by default, will be treated as an income stream payment and is exactly how most pensioners have treated it in the past. In this scenario, taking the excess as income stream payments each year doesn’t give the option to transfer more into pension at a future time.

Lump Sum

However, if an election is made to treat that $70k as a lump sum then it will create a $70k debit to the transfer balance cap. That then means that instead of using the full cap of $1.6 mil and not having the ability to put more money into pension at a later date, the person has utilised $1.53 mil and has $70k of the cap remaining. This may not sound like much, but after a few years it could potentially add up to a reasonable sum that allows an additional transfer of money into pension phase at a later date. Contrast that with several years of taking excess income stream payments and not having the ability to put more into pension at a later date if desired.

Does this apply to me if I have less than $1.6m?

Now, it may seem that this is only relevant for people that have at least $1.6 mil. While that might not be the position a retiree is in at this time there needs to be a consideration of what the situation may look like if, say, they became entitled to a reversionary pension which had the potential to exceed the cap, a potential inheritance or other money outside of super that they are able to contribute at a later date.

Managing the cap along the way will provide the most flexibility for the future.

How do I elect for a payment to be considered a lump sum?

To do so, an election must be made for the payment to be treated as a lump sum and not as a superannuation income stream benefit. The ATO stipulates that this election must be made before the payment takes place. If the election isn’t made, then the payment is treated as a normal pension payment. A lump sum payment from a pension account (that doesn’t clear the balance to nil) is a partial commutation of the pension.

We’ve added a template to our website, under Downloads & Forms that you can use to make this election. It can be found here:

Once the election has been completed and signed, the payment can be made. The original should be kept by the trustee and a copy of the signed election should be provided to us at that time. That will allow us to record it properly in the accounts and advise the ATO in the required timeframe (which is currently under review by the ATO and will be the subject of another article when finalised)

Can I take more than one lump sum during the year?

Yes, but each lump sum payment requires an election and possible notification to the ATO. From an administrative point of view keeping the number of lump sums to a minimum is desired, but that does not preclude you from taking more than one.

Lump sum from accumulation account may also be something to consider

So far, we’ve only considered taking the excess over the minimum pension payment as a lump sum from the pension account. If there is also an accumulation account that has the ability to have lump sums taken (i.e. it has unrestricted non preserved components) then that should be considered as well. A lump sum from the accumulation account won’t affect the transfer balance cap but it will reduce the amount in the fund that carries a less favourable tax consequence.

Scenario 2

Let’s say that the member is 65 and has $2.0 mil in super. Of that, $1.6 mil is in pension and $400k is in accumulation. They intend to withdraw $150k from the fund during the year. The minimum pension payment is $80k so at least $80k of that has to be treated as an income stream payment from the pension account. As per the previous example, the excess $70k could be treated as a lump sum from the pension account or as an income stream payment. In this case, it could also be treated as a $70k lump sum from the accumulation account. Here’s a table of what the 3 different options would look like:

$80k income stream; $70k lump sum from accumulation

$80k income stream; $70k lump sum from pension

$150k income stream from pension

Starting balance of pension

$1.6mil

$1.6mil

$1.6mil

Less income stream payment

-$80k

-$80k

-$150k

Less lump sum payment

-$0

-$70k

-$0

Closing balance of pension

$1.52mil

$1.45mil

$1.45mil

Starting balance of accumulation

$400k

$400k

$400k

Less lump sum payment

-$70k

-$0

-0

Closing balance of accumulation

$330k

$400k

$400k

Total balance in fund

Tax exempt portion of member’s balance (approx.)

$1.85mil

82.1%

$1.85mil

78.3%

$1.85mil

78.37%

Initial Transfer balance cap used

$1.6mil

$1.6mil

$1.6mil

Less lump sum

-$0

-$70k

-$0

Closing Transfer balance cap

$1.6mil

$1.53mil

$1.6mil

A Word of Caution

If you are going to elect to treat a payment as a lump sum, please ensure that you don’t count that payment as part of the minimum pension payment made for the year. Lump sums no longer count towards the minimum. If you include it by mistake in your calculations and then don’t take the minimum pension payment for the year, the pension will cease from the beginning of the year and the fund will lose the tax exemption on earnings supporting a pension. You cannot retrospectively change your mind and instead treat a lump sum as a normal income stream payment if you find that the minimum payments weren’t taken.

This is applicable for account based pensions and the new TRIS – in retirement phase for those people that have met a full condition of release. It is not relevant for people who are solely in accumulation or have a normal TRIS, market linked pension or defined benefit pension. Any personal tax consequences or effect on the tax-free/taxable components of the various balances has also not been considered in the examples provided.

This information is general in nature and should not be considered advice. We are not licenced to provide financial advice and cannot recommend whether a particular strategy would be appropriate to your circumstances. You may wish to seek the assistance of a licenced financial advisor for further information and advice.

The increase in the income threshold from 1 July 2017 may mean that it’s time to give the spouse superannuation tax offset a consideration for the 2017/18 year.

The spouse superannuation tax offset has been around for nearly 20 years but the income threshold to claim this offset has only recently been increased from $10,800.00 to $37,000.00 making it accessible to more people.

The offset is worth up to $540.00 for a contributing spouse that makes contributions into an eligible spouse’s superannuation account.

Here’s How It Works

An 18% offset is available for up to $3,000 in super contributions. The income threshold to receive the maximum offset is $37,000 with a gradual reduction to nil once the spouse’s assessable income reaches $40,001.

Example of Different Scenarios

*No additional benefit for spousal contributions over $3,000

The Nitty Gritty – Eligibility Criteria

As with most things that are tax related there are eligibility criteria that must be met. The aim of this offset is to provide a super tax concession to low-income earners and people with interrupted work patterns. Here is a summary of those that apply to this offset:

Spouse’s assessable income <$40,001 (full offset available if <$37,000 with a gradual reduction to nil at $40,001)

Note – assessable income is different to taxable income. It includes income before any deductions as well as total reportable fringe benefits and reportable employer super contributions.

Your spouse cannot have exceeded their non-concessional contribution cap for the year;

Your spouse cannot have a total superannuation balance equal to or exceeding the transfer balance cap (currently $1.6mil) immediately before the start of the financial year in which the contribution was made.

How Do I Claim the Offset?

To claim the spouse tax offset you need to complete the ‘Superannuation contributions on behalf of your spouse’ question in the supplementary section of your personal tax return. You also need to complete ‘Spouse details – married or de facto’ in your tax return.

Ensure to let the administrator of the super fund know how to treat the contribution.

Definition of Spouse

Reminder, too, that the definition of a spouse for ATO purposes is:

Another person (of any sex) who:

You were in a relationship with that was registered under a prescribed state or territory law; or

Although not legally married to you, lived with you on a genuine domestic basis in a relationship as a couple.

A desire for some people who exit large funds and start a new SMSF is to leave a portion of their superannuation in the large fund. This is often because it can be relatively simple to retain life, total and permanent disability (‘TPD’) and income protection insurance cover in a large fund.

While the above strategy broadly works, SMSF members need to be careful of traps in large funds that can cause a loss of cover. This article highlights some of the traps and pitfalls to look out for.

Keeping money in a big super fund

One of the perceived advantages in keeping a balance with a large superannuation fund is access to low cost insurance that has been arranged ‘in bulk’ by the superannuation fund. Often, no medical examinations are necessary to have access to this cover.

Despite any advantages, there can be terms in these insurance arrangements that cause cover to cease. This could be unexpected. Some of the circumstances we are aware of are outlined below.

No employer contributions

At a super fund known to us, if employer contributions cease for six months, a member automatically loses income protection cover. We understand that this is a policy for certain large funds that offer members automatic income protection insurance. In this vein, we are also aware of another large fund where income protection cover ceases after 13 months from the date of the last employer contribution, regardless of account balance. After 12 months (one month before the 13 month period expires), the fund notifies the member that cover is about to cease.

Not meeting minimum balance requirements

To retain cover at most large funds, the funds usually require that the member maintains a minimum balance in your account. From a review of a number of funds, this can be as low as $1,000 or as high as $10,000. While most large funds let members retain cover as long as premiums can be automatically deducted from their account, we are aware of a fund that will cease insurance cover for life, TPD and income protection when the account balance falls below $1,500 and no employer contributions are made after 12 months. This fund will contact the member to advise that cover will cease. Similarly, we are aware of other funds, including a fund that will cease life, TPD and income protection cover if the member’s account balance is below $2,000 and no employer contributions or rollovers are made for 12 consecutive months. Another fund will cease life and TPD cover six months from the end of the month from which the employer made a contribution to the member’s account and their balance is less than $1,200.

No longer working for a particular employer

Further, we are aware of a fund that requires that a particular employer (among a group of approved employers) makes contributions to the member account. At this fund, TPD and income protection cover cease without notice if the member is no longer working for that employer after 71 days and their account balance is less than $3,000.

No longer working in the corporate body or public sector

Some large funds cease insurance cover if the member no longer works with a particular employer or in a particular industry. This is a common feature of corporate and public sector superannuation funds. We are aware of some public sector funds where income protection cover ceases on the day the member officially ceases employment with the relevant public sector. There is also another public sector fund that will cease all cover after 60 days from the last employer contribution or when the member stops working in the relevant public sector. Additionally, these public sector funds generally do not accept further contributions or rollovers if the member is no longer working for the relevant public sector employer.

Membership in most corporate funds is for employees and former employees, and at certain funds this is extended to allow relatives of employees to join. We are aware of a corporate fund that automatically provides employees a corporate cover that would not otherwise be available to non-employees. However, membership at this corporate cover is only available to current employees. Hence, if the member stops working with the relevant employer connected to this corporate fund and does not have a minimum $1,200 balance with the fund, the corporate cover which includes life, TPD and income protection cover will cease 30 days after the member ceases employment.

Restrictions on terminal illness payouts

We are also aware of a certain fund whereby on terminal illness, the insurance can pay out at the TPD level (or a deemed TPD level), which could be lower than the amount of life cover. This payment reduces any remaining life cover paid on death. The effect of this may be a deprivation of funds to pay for medical or palliative care before death. This method of terminal illness cover stands in contrast to other funds that pay out 100% of life cover upon terminal illness.

This style of cover can also give rise to more tax because the beneficiaries will receive the death benefits, as opposed to the member receiving benefits before they die.

Staying informed

Be aware that some large funds may not give warning when insurance cover is about to cease. Therefore it is important to monitor accounts periodically.

Large super funds should have their insurance policies outlined in their insurance guide or product disclosure statement. These policies should be read carefully and any questions should be directed to the super fund for clarification on exactly how insurance cover applies.

Insurance in an SMSF

If the member no longer wishes to maintain insurance in a large super fund, or is unable to, it is of course possible to maintain certain kinds of insurance in an SMSF. Indeed, the law says that SMSF trustees must formulate, review regularly and give effect to an investment strategy that includes consideration of whether to hold a contract of insurance for one or more members of the fund.

This article is for general information only and should not be relied upon without first seeking advice from an appropriately qualified professional.

Note: DBA Lawyers hold SMSF CPD training at venues all around Australia and online. For more details or to register, visit www.dbanetwork.com.au or call 03 9092 9400.

The article is used with the permission of DBA Lawyers, Level 1, 290 Coventry Street

South Melbourne Vic 3205

10 March 2016

When is my First SMSF Annual Return due?

Annual returns for newly registered SMSFs (taxable and non-taxable) are due for lodgement by:

– 31 October 2016 for SMSFs who prepare their own annual return

– 28 February 2017 for SMSFs who are tax agent clients.

ATO Website extract :

You need to lodge an annual return once the audit of your SMSF has been finalised. The SMSF annual return is more than an income tax return. It is also used to report super regulatory information, member contributions and pay the SMSF supervisory levy.

If your fund did not have assets in the first year it was registered, it may not need a return lodged for that year.

You need to lodge an annual return once the audit of your SMSF has been finalised. The SMSF annual return is more than an income tax return. It is also used to report super regulatory information, member contribution data and payment of the supervisory levy.

Generally speaking, if your return is lodged each year through a tax agent and you have maintained a good lodgement record, the due date will be the 15th of May. For the first year the due date would be the 28th of February.

If you choose to lodge your SMSF annual return without the assistance of a tax agent, the due date for the first year is 31 October and changes to 28 Feb for subsequent years. If you did not lodge your return for the previous financial year on time the due date will be 31 October.

The above dates are a guide and should be read in conjunction with the ATO Key Lodgement dates:

Annual returns for new registrant (taxable and non-taxable) SMSFs are due for lodgement by:

• 31 October 2016 for SMSFs who prepare their own annual return

• 28 February 2017 for SMSFs who are tax agent clients.

Existing Self-Managed Super Funds (SMSFs)

Annual returns for existing (taxable and non-taxable) SMSFs are due for lodgement by:

• 28th February 2017 for SMSFs who prepare their own annual return

• 15th May 2017 for SMSFs who are tax agent clients.

Does my SMSF Trust Deed need stamping ?

This is a very good question and the requirements in relation to stamping a deed establishing a SMSF differs from state to state. Presently, the only jurisdictions in Australia that require stamping are Tasmania and the Northern Territory. None of the other jurisdictions require new SMSF trust deeds to be stamped